By

·

7 minute read

By

·

7 minute read

ESRS (European Sustainability Reporting Standards) is the EU's new set of rules for how companies report their environmental and social impacts. Starting January 2024, about 50,000 EU companies must follow these standards.

Here's what you need to know:

-

What: 12 detailed standards that tell companies exactly how to report sustainability data

-

Who: Large EU companies first (2024), then smaller ones by 2026

-

Why: Makes sustainability reporting consistent across the EU

-

Key Feature: Uses "double materiality" - companies must report both their impact on sustainability AND how sustainability issues affect their business

The standards cover:

-

Environmental impacts (like carbon emissions)

-

Social responsibility

-

Business governance

-

Financial risks from sustainability issues

Important Dates:

-

Large companies (250+ employees): Start 2024, first report 2025

-

Medium companies (€50M+ turnover): Start 2025, first report 2026

-

Listed SMEs: Start 2026, first report 2027

Bottom line: If you're a company operating in the EU, you'll need to track and report detailed sustainability data. Most companies (70%) find this challenging, so starting early with the right tools is key.

Related video from YouTube

What is ESRS?

The European Sustainability Reporting Standards (ESRS) are a framework introduced by the European Commission on July 31, 2023. They aim to make sustainability reporting consistent and comparable across the European Union. Through these standards, companies can better communicate their environmental, social, and governance (ESG) impacts transparently.

Breaking Down ESRS

The framework includes 12 detailed standards, split into two categories:

-

Cross-cutting standards: ESRS 1 and ESRS 2, which establish the foundation for broader ESG reporting.

-

Topical standards: Covering specific areas like climate change, pollution, and biodiversity.

"The ESRS aim to standardize and enhance the transparency of ESG reporting across Europe, ensuring that companies provide comprehensive and comparable sustainability information", explains the European Financial Advisory Group (EFRAG), which led the development of these standards.

The ESRS framework is designed to align with both global reporting systems and the EU’s Green New Deal and Sustainable Finance Framework. This dual alignment helps companies streamline their reporting processes across different regulatory and international requirements.

Why ESRS is Important for Businesses

ESRS introduces major changes for companies across the EU. Starting in January 2024, around 50,000 businesses must comply with these new requirements - a major shift in the way sustainability is documented and shared.

The standards impact businesses in several ways:

|

Focus Area |

How It Affects Companies |

|---|---|

|

Transparency |

Establishes a standard approach to communicate sustainability efforts effectively. |

|

Compliance |

Ensures companies meet EU regulatory mandates and CSRD obligations. |

|

Strategy |

Encourages integrating sustainability into broader business goals. |

To meet ESRS requirements, companies must perform materiality assessments and start embedding sustainability metrics into their operations. With sector-specific standards expected by June 2026, staying updated and ready for future changes will be increasingly important.

How ESRS and CSRD Work Together

The European Sustainability Reporting Standards (ESRS) and the Corporate Sustainability Reporting Directive (CSRD) create a unified framework for sustainability reporting across the EU. The CSRD sets the stage by defining who must report and when, while the ESRS provides a blueprint for how to meet compliance standards.

How ESRS Supports CSRD Rules

ESRS acts as the operational playbook for navigating CSRD obligations, offering approximately 1,191 detailed data points for organizations to track and disclose. It includes 12 key standards, designed to help companies align with CSRD guidelines:

|

Reporting Area |

How ESRS Assists with CSRD |

|---|---|

|

Environmental Impact |

Provides metrics for carbon emissions and energy use tracking |

|

Social Responsibility |

Sets guidelines for reporting on workforce and community outcomes |

|

Governance |

Outlines standards for oversight and ethical business practices |

"The ESRS is not a separate or competing entity working alongside the CSRD – they are the explanation of what, how and where companies need to report their ESG findings in order to comply with CSRD", according to EFRAG documentation.

Key Dates to Know

The rollout follows a phased timeline, allowing companies to adjust gradually:

|

Phase |

Who It Affects |

Start Date |

First Report Due |

|---|---|---|---|

|

Phase 1 |

Large listed EU companies (250+ employees) |

January 2024 |

2025 |

|

Phase 2 |

Other large companies (over €50M turnover) |

January 2025 |

2026 |

|

Phase 3 |

Listed small and medium enterprises (SMEs) |

January 2026 |

2027 |

A Baker Tilly study found that 88% of companies feel unprepared for the CSRD's requirements, stressing the need for early action. Take Royal Philips as an example: after conducting a double-materiality assessment in 2022, they realized they were just 30% compliant with CSRD and ESRS expectations. This discovery prompted them to form a dedicated CSRD steering committee to close the gaps.

Main Parts of ESRS

The European Sustainability Reporting Standards (ESRS) consist of 12 interconnected standards, creating a structured framework for sustainability reporting. These rules, which took effect in January 2024, apply to roughly 50,000 companies operating within the European Union.

General and Climate Reporting Standards

The ESRS framework is anchored by two key cross-cutting standards that guide all sustainability reporting efforts:

|

Standard |

Purpose |

Key Requirements |

|---|---|---|

|

ESRS 1 |

General Principles |

Establishes reporting boundaries and provides guidelines for materiality assessment |

|

ESRS 2 |

Disclosure Requirements |

Defines essential information for sustainability reports |

|

ESRS E1-E4 |

Environmental Standards |

Addresses climate change, pollution, water resources, and biodiversity |

Among these, ESRS E1 takes a central role by focusing on climate-related disclosures. Companies using this standard must report their greenhouse gas emissions, outline their climate-related targets, and share detailed transition plans for reducing carbon emissions.

What is Double Materiality?

Double materiality stands at the heart of ESRS, requiring organizations to evaluate sustainability risks and opportunities through two lenses:

|

Materiality Aspect |

Focus Area |

Reporting Requirements |

|---|---|---|

|

Impact Materiality |

Environmental and social effects |

Examines how a company’s operations influence the planet and people |

|

Financial Materiality |

Business risks and opportunities |

Evaluates how sustainability issues affect the organization’s financial results |

"The ESRS framework aims to provide a transparent, accurate, and comparable view of a company's ESG impacts, risks, and opportunities", states the European Commission's official documentation from July 2023.

This dual-perspective approach ensures organizations consider both how they affect sustainability goals and how sustainability challenges could influence their financial health. For instance, under ESRS E1, a company would need to disclose not only its carbon emissions but also how climate-related risks might disrupt its business strategy and economic stability.

Why Carbon Accounting is Important for ESRS

Carbon accounting plays a key role in meeting ESRS E1 requirements, helping companies track and report their greenhouse gas emissions. Under the standards adopted by the European Commission in July 2023, businesses are expected to document emissions across their entire value chain in detail.

Reporting Scope 1, 2, and 3 Emissions

Under ESRS E1, companies must report emissions across three main categories:

|

Description |

Reporting Requirements |

|

|---|---|---|

|

Scope 1 |

Direct emissions |

Emissions from company-owned facilities and vehicles |

|

Scope 2 |

Indirect energy emissions |

Emissions from purchased electricity, heating, and cooling |

|

Scope 3 |

Value chain emissions |

Emissions tied to supplier activities, product use, and end-of-life disposal |

The first ESRS reports, due in 2025, will require businesses to provide detailed data showing their greenhouse gas emissions and related financial risks. This aligns with the "double materiality" principle central to the framework.

Challenges in Collecting Carbon Data

Accurate carbon data collection for ESRS compliance comes with unique challenges. These include:

|

Challenge Area |

Impact |

Solution Approach |

|---|---|---|

|

Data Accuracy |

Inconsistent methods for measuring emissions |

Use standardized GHG Protocol calculations |

|

Supply Chain Complexity |

Tracking indirect (Scope 3) emissions is difficult |

|

|

Resource Requirements |

Gathering data needs time and expertise |

Implement specialized carbon accounting software |

"The ESRS framework aims to provide a transparent, accurate, and comparable view of a company's ESG impacts, risks, and opportunities", the European Commission notes, underlining the importance of precise carbon data.

Sector-specific standards arriving by June 2026 will likely introduce additional carbon accounting requirements. To stay ahead, businesses should prioritize reliable data collection systems that are flexible enough to meet future needs while ensuring transparency and accuracy.

Tools to Help with ESRS Reporting

EY's 2023 report highlights that 70% of companies face challenges collecting and managing sustainability data. In this context, specialized software has become a go-to for handling ESRS compliance efficiently. These tools not only make reporting smoother but also improve accuracy and completeness.

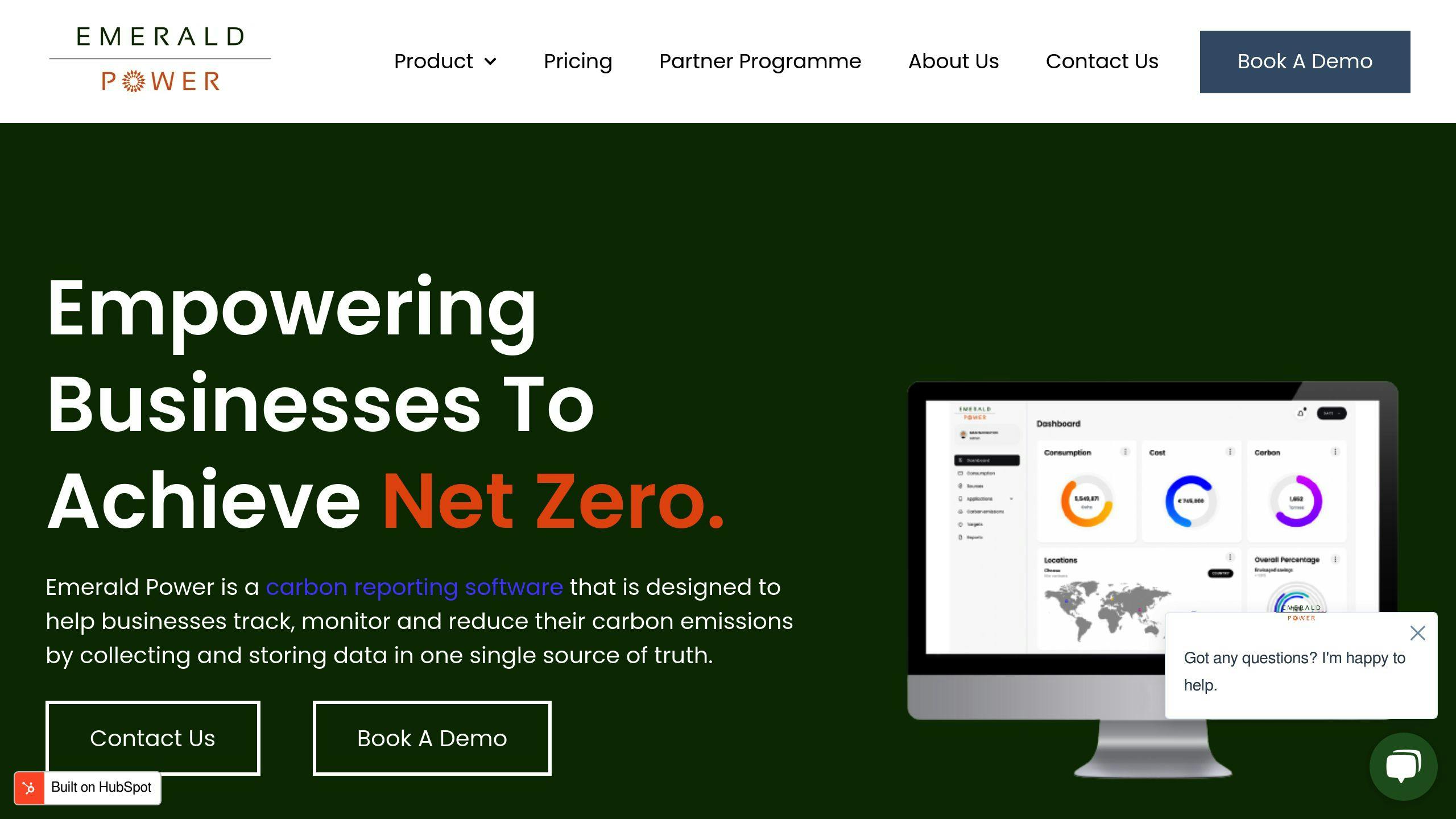

Using Emerald Power for Carbon Reporting

Emerald Power offers carbon accounting software tailored specifically for mid-sized businesses preparing for CSRD compliance. Here's what you can expect:

|

Feature |

How It Helps with ESRS Reporting |

|---|---|

|

Automated Data Collection |

Minimizes manual errors and saves time with direct system integrations |

|

Keeps you on top of emissions data and allows swift action on sustainability goals |

|

|

Ensures reporting meets established standards |

|

|

Multi-location Management |

Simplifies data handling across various offices or regions |

How Software Simplifies ESRS Reporting

Modern platforms for sustainability reporting are designed to solve common ESRS hurdles through automation and intelligent tools. For instance, Sweep has reduced audit processing times by 50%, helping firms stay compliant and avoid penalties.

|

Reporting Challenge |

How Software Helps |

|---|---|

|

Data Collection |

Automates input from diverse systems and sources |

|

Accurate Calculations |

Pre-built GHG Protocol formulas and real-time verification features |

|

Tracking Progress |

Provides dashboards and notification systems to monitor key metrics |

|

Managing Documentation |

Centralizes files and creates consistent audit trails |

"The ESRS will help hold companies accountable to the EU's goals for climate neutrality by 2050 and the transition to a more just and sustainable economy", the European Commission explains, emphasizing the importance of strong reporting mechanisms.

With sector-specific standards on the horizon by June 2026, adopting these tools sooner rather than later can ease current reporting efforts and set businesses up for future compliance. Effective software not only meets today's needs but also builds a reliable framework for the years ahead.

Conclusion

Key Takeaways

The European Sustainability Reporting Standards (ESRS) bring a major change to how companies report sustainability practices across the EU. This framework, featuring 12 detailed standards, gives clear directions for transparent ESG reporting. When the European Commission officially adopted ESRS on July 31, 2023, it marked an important moment in streamlining sustainability reporting.

A unique aspect of ESRS is its double materiality approach. This means companies must evaluate not only how they affect sustainability issues but also how these issues influence their business. This dual focus provides a broader understanding of both sustainability efforts and risks at the corporate level.

|

Timeline Milestone |

Implementation Phase |

|---|---|

|

July 2023 |

Initial ESRS adoption |

|

2024 |

First reporting year for large companies |

|

June 2026 |

Sector-specific standards implementation |

Steps for Businesses to Get Ready

To comply with ESRS, businesses must act promptly. With tight timelines, especially for those covered by the CSRD, it's crucial to focus on certain key areas:

|

Action Area |

Implementation Strategy |

|---|---|

|

Data Systems |

Introduce automated systems for data collection and checks |

|

Reporting Framework |

Update internal processes to meet ESRS guidelines |

|

Carbon Accounting |

Build robust tools for tracking emissions across all scopes |

|

Technology Integration |

Use specialized software to simplify reporting processes |

"The ESRS framework is designed to provide a clear and comprehensive framework for sustainability reporting, facilitating transparency, comparability, and accountability while driving the transition to a sustainable economy", says the European Commission, highlighting its broader goal of climate neutrality by 2050.

With 70% of companies facing challenges in managing sustainability data, investing in the right tools and strategies now can make compliance much more manageable. Treat ESRS as a chance to strengthen your sustainability approach while contributing to the EU’s environmental initiatives.

FAQs

What is the purpose of the ESRS?

The European Sustainability Reporting Standards (ESRS) provide a structured framework to unify sustainability reporting across the EU. Officially adopted by the European Commission on July 31, 2023, the ESRS features 12 in-depth standards covering environmental, social, and governance (ESG) topics. This framework ensures businesses report their sustainability efforts clearly and uniformly.

"The ESRS is designed to provide a clear and comprehensive framework for sustainability reporting, integrating sustainability into corporate strategy and communication", explains PlanA.Earth, emphasizing the importance of these standards.

Does ESRS require scope 3?

Yes, scope 3 emissions reporting is a clear requirement under the ESRS. Specifically, ESRS E1 (Climate Change) mandates companies to report their full greenhouse gas emissions profile. This includes:

-

Scope 1: Direct emissions.

-

Scope 2: Indirect emissions from purchased energy.

-

Scope 3: Emissions across the entire value chain.

This aligns with the GHG Protocol approach and ensures organizations account for emissions at every level.

.png?width=820&height=312&name=Book%20Your%20Prince2%20Training%20(1).png)

|

Emission Scope |

Reporting Requirement |

Implementation Timeline |

|---|---|---|

|

Scope 1 & 2 |

Mandatory, immediate reporting |

Starting 2024 for large companies |

|

Scope 3 |

Required as per GHG Protocol |

Phased implementation based on company size |

|

Sector-specific |

Additional pending criteria |

Expected by June 2026 |