What Are Scopes 1, 2 and 3 Emissions? The Ultimate Guide (2026)

Quick Summary: Scope 1, 2 and 3 emissions are the three categories the GHG Protocol uses to classify a company's greenhouse gas footprint. Scope 1 covers direct emissions from sources you own or control (company vehicles, boilers, on-site fuel use). Scope 2 covers indirect emissions from the electricity, steam, heat or cooling you purchase. Scope 3 covers everything else in your value chain — 15 categories spanning purchased goods, business travel, commuting, logistics, product use and end-of-life. For most organisations, Scope 3 represents 70–95% of total emissions, which is why regulators (CSRD, UK SRS, California SB 253) and frameworks like SBTi and EcoVadis now expect it to be measured, even though it remains the hardest scope to calculate. This guide breaks down every category, gives you 2025/2026 emission factor and regulation updates, shows you how to calculate each scope, and explains how to start reducing them.

What Is the GHG Protocol, and Why Do Emissions Have "Scopes"?

The Greenhouse Gas (GHG) Protocol is the global accounting standard for measuring and reporting greenhouse gas emissions. It was developed jointly by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), and its Corporate Accounting and Reporting Standard underpins virtually every climate disclosure framework in use today — including CSRD/ESRS, the UK's SECR and UK SRS, California's SB 253, the ISSB's IFRS S2, CDP, and SBTi target-setting.

The "scopes" exist to solve one specific problem: avoiding double-counting while still capturing a company's full climate impact. A litre of diesel burned in a delivery van is Scope 1 for the haulage company that owns the van, but Scope 3 (transportation and distribution) for the manufacturer whose goods are on board. By dividing emissions into three scopes, the GHG Protocol lets every organisation in a value chain report its emissions without the same tonne of CO₂ being claimed twice in a national inventory.

Direct answer: Scope 1, 2 and 3 are the three categories of greenhouse gas emissions defined by the GHG Protocol Corporate Standard. Scope 1 = direct emissions you control. Scope 2 = indirect emissions from purchased energy. Scope 3 = all other indirect emissions across your value chain.

Scope 1, 2 and 3 at a Glance

| Scope 1 | Scope 2 | Scope 3 | |

| Definition | Direct emissions from owned or controlled sources | Indirect emissions from purchased electricity, steam, heat and cooling | All other indirect emissions across the value chain (upstream and downstream) |

| Control level | High — directly controllable | Medium — controllable via supplier/tariff choice | Low — depends on suppliers, customers, employees |

| Typical examples | Company vehicles, gas boilers, on-site generators, refrigerant leaks | Electricity for offices, warehouses, data centres; purchased heat/cooling | Purchased goods, business travel, commuting, logistics, waste, use of sold products |

| Number of categories | 4 sub-categories | 2 reporting methods (location-based, market-based) | 15 categories (8 upstream, 7 downstream) |

| Reporting status | Mandatory under nearly all frameworks | Mandatory under nearly all frameworks | Increasingly mandatory, but often phased in with relief periods |

| Typical share of total footprint | Often 5–15% | Often 2–10% | Typically 70–95% |

| Difficulty to measure | Low–Medium | Low | High |

| GHG Protocol guidance status (2026) | Stable (Corporate Standard, 2004/2015 amendments) | Under first major revision since 2015 — final standard due 2027 | Under Phase 1/Phase 2 revision of the 2011 Scope 3 Standard |

Scope 1 Emissions Explained

Scope 1 emissions are direct greenhouse gas emissions from sources that a company owns or controls. If your business burns the fuel, operates the equipment, or leaks the gas itself, it's Scope 1. This is the only scope where a company has near-total operational control, which is why it's usually the starting point for any decarbonisation plan.

The GHG Protocol splits Scope 1 into four sub-categories:

The Four Categories of Scope 1 Emissions

| Category | What it covers | Common examples | Notes |

| 1. Stationary combustion | Fuel burned in fixed equipment on-site | Natural gas boilers, oil-fired heating, on-site generators, furnaces | The single largest Scope 1 source for most office-based and light-industrial businesses |

| 2. Mobile combustion | Fuel burned in vehicles owned or leased by the company | Company cars, vans, HGVs, forklifts, company-owned ships or aircraft | Electric vehicles charged on-site shift this emission into Scope 2 instead |

| 3. Fugitive emissions | Unintentional leaks of greenhouse gases | Refrigerant leaks from air conditioning and refrigeration units (HFCs), SF₆ from electrical switchgear | Refrigerants can have a global warming potential hundreds to thousands of times that of CO₂, so even small leaks matter |

| 4. Process emissions | Emissions released during physical or chemical industrial processes | Cement calcination, chemical manufacturing, metal smelting, on-site waste incineration | Most relevant to manufacturing, heavy industry and process-based businesses |

Real-World Scope 1 Examples

- A logistics company's diesel-fuelled delivery fleet

- A manufacturer's natural gas-fired ovens or kilns

- A restaurant's gas hobs and on-site fryers

- A data centre's diesel backup generators

- An office's leaking air conditioning refrigerant

- A farm's on-site fuel use for machinery

Key takeaway: Scope 1 is the only scope where reduction is entirely within your own decision-making — switching fuels, electrifying fleets, improving combustion efficiency, and managing refrigerants directly lowers your Scope 1 number.

Scope 2 Emissions Explained

Scope 2 emissions are indirect greenhouse gas emissions from the generation of electricity, steam, heating or cooling that a company purchases and consumes. The emissions physically occur at the power station or energy supplier — not on your premises — but they exist because of your energy demand, so the GHG Protocol attributes them to you.

For most SMEs and office-based companies, purchased grid electricity is the dominant — often the only — source of Scope 2 emissions.

Location-Based vs Market-Based Reporting

Since the 2015 Scope 2 Guidance, companies must report Scope 2 using two parallel methods:

| Method | How it's calculated | What it reflects | Best for |

| Location-based | Average emissions intensity of the grid(s) where your electricity is consumed | The physical reality of the grid mix in your region | Comparability between companies in the same area |

| Market-based | Emissions based on the specific energy contracts you've purchased (e.g. renewable energy certificates, Guarantees of Origin, PPAs) | Your actual procurement choices | Showing the impact of buying renewable electricity |

A company can have a high location-based figure (because its national grid is carbon-intensive) but a low market-based figure (because it has purchased certified renewable electricity) — or vice versa. Both figures must be disclosed under most current frameworks.

The 2025–2027 GHG Protocol Scope 2 Overhaul

This is the single biggest change coming to Scope 2 accounting in a decade, and any "ultimate guide" written after 2025 needs to cover it:

- The Scope 2 Guidance (2015) is undergoing its first major revision. A 60-day public consultation ran from 20 October 2025 to 31 January 2026, with a second consultation expected later in 2026.

- The most significant proposed change is hourly matching: contractual instruments like Renewable Energy Certificates (RECs), Guarantees of Origin (GOs) and Power Purchase Agreements (PPAs) would need to match electricity consumption to the hour and grid region in which it occurs — not simply matched annually as is permitted today.

- The location-based method would also be updated with a new emission factor hierarchy and a requirement to use the most granular factors accessible.

- The revision will be published as a full Standard (not just "Guidance"), with final publication expected in 2027.

- A related, separate consultation on consequential / system-wide accounting (estimating avoided emissions from electricity-sector actions) ran in parallel.

What this means for you: if your business currently relies on annually matched renewable energy certificates to report a low market-based Scope 2 figure, that approach may become significantly harder to defend after 2027. Businesses procuring renewable electricity should start tracking when and where that electricity is generated relative to their own consumption.

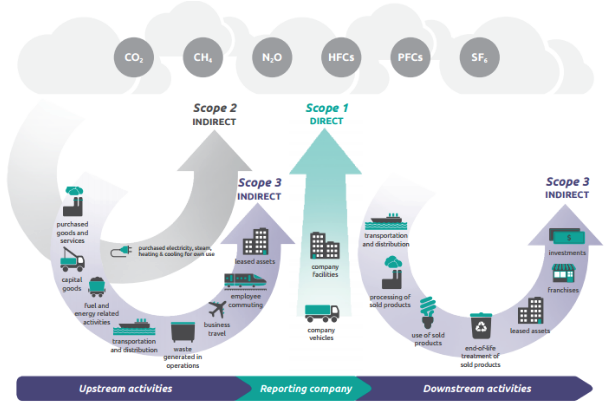

Scope 3 Emissions Explained — All 15 Categories

Scope 3 emissions are all indirect greenhouse gas emissions that occur in a company's value chain — both upstream (supply chain) and downstream (customers and product end-of-life) — that are not already captured in Scope 1 or Scope 2. The GHG Protocol's Corporate Value Chain (Scope 3) Standard, published in 2011, defines 15 distinct categories, split into upstream and downstream activities.

This is the scope most articles gloss over — but it's almost always where the bulk of a company's climate impact (and climate risk) actually sits.

The 15 Scope 3 Categories

| Number | Category | Upstream / Downstream | What it covers | Typical examples |

| 1 | Purchased goods & services | Upstream | Cradle-to-gate emissions of everything bought in the reporting year | Raw materials, components, office supplies, software, professional services |

| 2 | Capital goods | Upstream | Emissions from production of capital assets, fully accounted in the year of purchase | Buildings, machinery, vehicles, IT hardware, equipment |

| 3 | Fuel & energy-related activities | Upstream | Emissions from producing fuels/energy not already counted in Scope 1 or 2 | Well-to-tank emissions of fuel, transmission & distribution (T&D) losses from purchased electricity |

| 4 | Upstream transportation & distribution | Upstream | Transport and logistics of purchased goods (before they reach you) | Inbound freight, third-party warehousing, supplier logistics |

| 5 | Waste generated in operations | Upstream | Disposal and treatment of waste produced by your operations | Landfill, recycling, incineration, wastewater treatment |

| 6 | Business travel | Upstream | Employee travel for business purposes in vehicles not owned/operated by the company | Flights, trains, taxis, rental cars, hotel stays |

| 7 | Employee commuting | Upstream | Employee travel between home and work | Car, public transport, cycling, walking; remote working impacts |

| 8 | Upstream leased assets | Upstream | Operation of assets leased by the reporting company (if not already in Scope 1/2) | Leased office space, leased vehicles, leased equipment |

| 9 | Downstream transportation & distribution | Downstream | Transport and distribution of sold products after they leave your control | Outbound logistics, retail distribution, third-party storage |

| 10 | Processing of sold products | Downstream | Further processing of intermediate products by downstream companies | A component manufacturer's part being assembled into a final product |

| 11 | Use of sold products | Downstream | Emissions from end-use of goods and services sold | Energy consumed by a sold appliance, fuel burned by a sold vehicle over its lifetime |

| 12 | End-of-life treatment of sold products | Downstream | Disposal/treatment of sold products at end of life | Landfill, recycling, incineration of products after consumer use |

| 13 | Downstream leased assets | Downstream | Operation of assets owned by the reporting company but leased to others | A landlord's leased commercial property |

| 14 | Franchises | Downstream | Operations of franchisees under the reporting company's brand | Franchise outlets' Scope 1 and 2 emissions |

| 15 | Investments | Downstream | Emissions associated with investments (equity, debt, project finance) | Portfolio company emissions, financed emissions — central to financial institutions |

How Scopes 1, 2 and 3 Fit Together in a Value Chain

Think of a simple product value chain — say, a piece of furniture:

Raw materials (timber, metal, foam) are extracted and processed — emissions here are Scope 3 Category 1 and 2 for the furniture company, but Scope 1 and 2 for the raw material supplier.

Inbound freight of those materials to the factory — Scope 3 Category 4 for the furniture company.

Manufacturing — fuel burned on-site is Scope 1; electricity used in the factory is Scope 2.

Outbound distribution to retailers — Scope 3 Category 9.

Retail operations — Scope 1/2 for the retailer, but Scope 3 Category 1 (purchased goods) for the furniture company from the retailer's perspective.

Use of the furniture — typically minimal for furniture, but Scope 3 Category 11 for products like appliances or vehicles, this can dwarf everything else.

End-of-life — disposal or recycling of the furniture is Scope 3 Category 12.

This is the mechanism by which the same physical tonne of carbon shows up as Scope 1 for one company and Scope 3 for another — and why collaboration across the value chain (supplier engagement, customer education, product design) is central to any credible Scope 3 reduction strategy.

The 2026 Regulatory Landscape for Scope 1, 2 & 3 Reporting

2025 and early 2026 brought the most significant regulatory shake-up to corporate carbon reporting in years — particularly in the EU, where the Omnibus I simplification package substantially narrowed who has to report, while the UK published its own standards for the first time. Here's where things stand as of mid-2026:

CSRD After the Omnibus: What Actually Changed

The Omnibus I Directive (Directive (EU) 2026/470) was approved by the European Parliament in December 2025, adopted by the Council on 24 February 2026, and entered into force on 18 March 2026. The headline changes for Scope 1, 2 and 3 reporting:

- CSRD scope dramatically narrowed: only EU undertakings with more than 1,000 employees AND net turnover above €450 million remain subject to mandatory ESRS reporting.

- Listed SMEs are fully exempt — a major shift from the original framework, which would have brought thousands of smaller listed companies into scope from 2026.

- Comprehensive value chain mapping requirements have been removed. Companies with 1,000 employees or fewer cannot be asked for sustainability data beyond what's in upcoming "voluntary standards," which the European Commission must define by 19 July 2026 — these are expected to be limited to essential, readily accessible information (broadly VSME-aligned).

- Timelines pushed back: in-scope EU large companies (the former "Wave 2") now report from FY2027; non-EU entities (the former "Wave 3" equivalent) from FY2028.

- A review clause means thresholds could be revisited again in future — so don't assume today's scope is permanent.

What this means in practice: even though far fewer companies are now legally required to produce a full ESRS report, the demand for Scope 1, 2 and 3 data flowing down supply chains hasn't disappeared — it's simply shifted from "comprehensive mandatory disclosure" to "streamlined data requests from large customers using voluntary standards." If you supply a company that remains in CSRD scope, expect requests for your Scope 1, 2 and (increasingly) Scope 3 data to continue, just in a lighter-touch format.

UK Sustainability Reporting Standards (UK SRS)

The UK published its finalised UK SRS S1 (general requirements) and UK SRS S2 (climate-related disclosures) on 25 February 2026 — based on the ISSB's IFRS S1 and S2 standards, with UK-specific amendments. Key points:

- Both standards are currently available for voluntary use.

- UK SRS S2 requires disclosure of Scope 1, 2 and 3 GHG emissions, climate-related financial metrics, scenario analysis, and progress against targets.

- The FCA's consultation (CP26/5) on making UK SRS mandatory for premium and standard listed companies closed 20 March 2026, with a policy statement expected autumn 2026 and an application date around 1 January 2027.

- Scope 3 gets a comply-or-explain runway with a one-year transitional relief; broader UK SRS S1 disclosures carry a two-year transitional relief.

- The standards incorporate ISSB amendments from December 2025, including the exclusion of certain Scope 3 categories from reporting requirements in initial application.

- The government is separately considering how UK SRS-based energy and emissions reporting interacts with SECR, aiming to reduce duplication for businesses already reporting under both.

US Developments: California SB 253 and Beyond

California's Climate Corporate Data Accountability Act (SB 253) remains one of the most consequential climate disclosure laws globally, precisely because — unlike the EU and UK frameworks — it applies to private as well as public companies, and explicitly requires Scope 3 reporting:

- CARB (California Air Resources Board) unanimously approved final implementing regulations on 26 February 2026.

- Companies with over $1 billion in annual revenue doing business in California (an estimated 5,000+ entities, many headquartered outside California or even outside the US) must report Scope 1 and Scope 2 emissions by 10 August 2026 (covering FY2025 data).

- Scope 3 reporting follows from 2027.

- Assurance requirements escalate over time: limited assurance for Scope 1/2 from 2026, moving to reasonable assurance from 2030, with limited assurance also eventually required for Scope 3.

- Litigation continues (the US and California Chambers of Commerce challenged both SB 253 and companion law SB 261), but the SB 253 reporting deadline has not been enjoined — companies should proceed on the assumption that the August 2026 deadline stands.

- New York is following California's lead: a Climate Corporate Data Accountability Act passed the NY Senate in February 2026 and, if enacted, would require Scope 1/2 reporting from 2028 and Scope 3 from 2029 for companies over $1bn in revenue.

How to Calculate Your Scope 1, 2 and 3 Emissions

The core formula behind almost every emissions calculation is the same:

Activity Data × Emission Factor = GHG Emissions (in kg or tonnes CO₂e)

Step-by-Step Approach

- Define your organisational and operational boundaries. Decide which entities/sites you're reporting for (equity share, financial control, or operational control approach) and which scopes/categories apply.

- Set a base year. This becomes your benchmark for measuring future reductions.

- Collect activity data for Scope 1. Fuel invoices (litres of diesel, m³ of gas), refrigerant top-up records, vehicle mileage logs.

- Collect activity data for Scope 2. Electricity bills (kWh), and details of any renewable energy contracts (for market-based reporting).

- Identify your material Scope 3 categories. Start with the 3–5 categories most relevant to your sector (see the sector table above).

- Gather Scope 3 activity data. Supplier spend data (for a spend-based approach), travel booking exports, employee commuting surveys, waste contractor reports, freight data.

- Apply the correct emission factors for the reporting year and region (e.g. DEFRA/DESNZ for UK activities, SEAI for Irish electricity, EPA for US activities, IEA for global aviation).

- Convert everything to CO₂e and sum by scope and category.

- Document your methodology — which emission factor dataset, which year, which calculation approach (spend-based vs activity-based vs supplier-specific) — so it's auditable and repeatable.

- Set targets and a reduction plan based on your baseline.

Common Mistakes Companies Make With Scope 1, 2 & 3

- Stopping at Scope 1 and 2 because they're easier — and missing the 70–95% of the footprint that sits in Scope 3.

- Using outdated emission factors. The UK's grid electricity factor alone fell ~14.5% in the 2025 dataset — using last year's factors can materially overstate (or understate) your Scope 2 figure.

- Double-counting between Scope 1 and Scope 3. A company-owned vehicle is Scope 1; the same vehicle, if leased and operated by a third-party logistics provider on your behalf, is Scope 3 Category 4 or 9.

- Treating market-based Scope 2 as "solved" with annually matched RECs. This is precisely the practice the GHG Protocol's 2025–2027 revision is tightening through hourly and regional matching requirements.

- Ignoring materiality guidance. Trying to perfectly calculate all 15 Scope 3 categories with equal rigour, instead of focusing effort on the 3–5 categories that actually matter for your sector.

- Inconsistent boundaries year to year. Switching calculation methods or organisational boundaries without restating prior years makes year-on-year comparisons meaningless.

- Not documenting methodology. Without a clear record of which emission factors, base year, and calculation approach were used, your figures can't be audited or assured — a growing requirement under SB 253, CSRD, and UK SRS.

- Assuming "we're too small to need this." Even where a business sits outside mandatory CSRD, UK SRS, or SB 253 thresholds, its larger customers, banks, and investors increasingly request Scope 1–3 data as part of their own (now VSME-aligned) supply chain reporting.

FAQs: Scope 1, 2 and 3 Emissions

What are Scope 1, 2 and 3 emissions in simple terms?

Scope 1 is direct emissions from things you own or control (like company vehicles and on-site boilers). Scope 2 is indirect emissions from the electricity, heat, steam or cooling you buy. Scope 3 is every other indirect emission across your value chain — from purchased goods to business travel to how customers use and dispose of your products.

Which scopes are mandatory to report?

Scope 1 and Scope 2 are mandatory under nearly every major framework, including CSRD/ESRS, UK SECR, UK SRS, and California SB 253. Scope 3 is increasingly mandatory but is often phased in with materiality assessments, comply-or-explain provisions, or transitional relief periods — for example, UK SRS currently provides a one-year transitional relief for Scope 3.

Why is Scope 3 considered the most important scope?

Because for most companies it represents the largest share of total emissions — on average around 75% across sectors, according to CDP, and as much as ~90–99% for sectors like capital goods and financial services. It's also where most of the genuine reduction opportunity (and supply chain risk) lies.

Do small businesses need to calculate Scope 3 emissions?

Most SMEs are not yet legally required to disclose full Scope 3 inventories under current EU, UK or US thresholds — especially after the EU's Omnibus I changes narrowed CSRD's scope. However, SMEs in the supply chains of larger companies are increasingly asked for Scope 1, 2 and 3 data as part of those larger companies' own (now more streamlined, VSME-aligned) reporting — so having this data ready is a practical commercial advantage even without a direct legal mandate.

What's the difference between location-based and market-based Scope 2 reporting?

Location-based Scope 2 uses the average emissions intensity of the grid where your electricity is consumed. Market-based Scope 2 reflects the specific energy contracts and certificates (like renewable energy certificates or PPAs) your company has purchased. Most frameworks require both figures to be disclosed side by side.

How is the GHG Protocol Scope 2 Guidance changing?

The Scope 2 Guidance (2015) is undergoing its first major revision, with a public consultation that ran from October 2025 to January 2026. The headline proposed change is "hourly matching" — requiring renewable energy purchases to be matched to the hour and grid region of consumption, rather than matched annually. The final revised standard is expected in 2027.

What emission factors should I use for 2026 reporting?

For UK-based activities occurring in 2025, use the UK Government (DESNZ/Defra) GHG Conversion Factors for Company Reporting, 2025 edition (published June 2025), which includes a sharply reduced grid electricity factor (down roughly 14.5% on 2024) and revised aviation, EV, and waste factors. For Irish electricity, use SEAI's published Irish grid emission factors. Always match the factor year to the year the emissions actually occurred.

Has CSRD been scrapped?

No — CSRD still exists, but the Omnibus I Directive (in force from 18 March 2026) dramatically narrowed its scope. Only EU companies with more than 1,000 employees and over €450 million in net turnover remain in mandatory scope, with reporting starting from FY2027. Listed SMEs are now exempt, and a simplified "voluntary standard" (broadly VSME-aligned) is being developed for smaller companies by mid-2026.

Does California's SB 253 really require Scope 3 reporting from private companies?

Yes. SB 253 applies to both public and private entities with over $1 billion in annual revenue doing business in California — an estimated 5,000+ companies. Scope 1 and 2 reporting is due by 10 August 2026 (covering FY2025), with Scope 3 reporting following from 2027.

What is Scope 4?

"Scope 4" is an informal term for avoided emissions — climate benefits a product or service creates outside a company's value chain (e.g. an energy-efficient product reducing emissions elsewhere). It isn't part of the official GHG Protocol scopes and should never be subtracted from a Scope 1–3 inventory; it's best understood as a supplementary, product-level claim.

How often do emission factors change?

In the UK, the DESNZ/Defra conversion factors are updated annually, typically published each summer (the 2025 edition, covering the 2025 calendar year, was published in June 2025). Significant year-on-year changes — such as the ~14.5% drop in the UK grid electricity factor for 2025 — mean carbon footprints can shift even when activity levels stay flat, simply because the underlying grid or fuel mix has become cleaner.